Connecting the Emerging Markets: China's Growing Role in Global Digital Infrastructure

HKUST IEMS Thought Leadership Brief No. 26

SHARE THIS

-

Rising demand for international communications drive cable capacity growth, yet financing and political risks remain major obstacles.

- Chinese investments help finance cable systems in multiple emerging market regions.

-

Emerging economies need to develop robust domestic regulations and international coordination to reduce political risks, protect cable infrastructure, and manage cyber risks.

Issue

Digital connectivity is the cornerstone for growth in the 21st Century. A 2009 World Bank report found that for every 10 percent increase in high-speed internet connections, there is a 1.3 percent increase in economic growth. Ninety-nine percent of international telecommunications transit through submarine cables. The lack of resilient digital infrastructure creates a bottleneck to economic development for emerging markets. China is eager to expand its own international communications network and tap into other markets to meet their growing infrastructure needs. This brief analyzes the rising demand for cable infrastructure and obstacles to infrastructure growth, and China’s growing role in the cable industry. It also recommends how emerging economies can enhance international connectivity and address related vulnerabilities.

Assessment

Rising demand for international communications infrastructure

Since the first cable across the English Channel in 1850, submarine cables have served as backbones for international communications. After the 1990s telecom investment boom and the 2000s market downturn, a resurgence came in this decade. The mass adoption of smartphones and cloud computing, and the growing ubiquity of broadband create surging international data demand. According to Submarine Telecoms Forum (STF), since 2014 the industry has added on average over 25 percent capacity (including new systems and upgrades) annually on major cable routes. Major growth occurred in intra-Asia, EMEA (Europe, Middle East, and Africa), and Latin America routes. Key factors driving capacity growth in emerging markets include rising capacity demand, government policy, multilateral development banks (MDB) financing, resiliency concerns and technology advancement (Figure 1).

Obstacles for new infrastructure development

Financing remains the primary obstacle to cable growth, as submarine cables are capital intensive projects with highly uncertain future returns over the long term of operation. The telecom industry lacks risk reduction schemes seen in other types of infrastructure. For example, energy pipeline projects can hedge against price risk using futures contracts. Consortia ownership has diffused risks to each participant, with each investing in a small proportion of total capacity to start and sharing the cost of construction and operation. There is, however, a significant upfront cash flow commitment, and coordination can be a challenge as all parties need to agree to any changes. Private ownership using the traditional project finance structure relies on sales to third parties like carriers to repay debt used to finance construction. It has comparably higher risks, due to uncertainties in securing capacity purchasers, fluctuations in future bandwidth pricing, and exchange rate and interest rate fluctuations. Investors may also seek financing from sources such as equipment suppliers, commercial banks, multilateral development banks (MDBs), private equity and venture capital.

Submarine cables are a critical transnational infrastructure that passes through waters with competing uses such as fishing, shipping, offshoring drilling, and military operations, so political risks can affect investment screening and permissions for cable landing and routing. For instance, foreign-invested cables landing in the United States need to be approved by the Federal Communications Commission, the Committee on Foreign Investment (CFIUS), and regulators from the Department of Homeland Security, Department of Justice, Federal Bureau of Investigation, and Department of Defense collectively known as Team Telecom. As an example, the licensing process for the TransPacific Express Cable (TPE) took 11 months. In emerging markets, inefficient regulatory structures may also lead to lengthy approval processes. For instance, according to Optic Marine Services, permits in Southeast Asia can take between 4 and 18 months. On the other hand, regulatory efficiency has attracted investors to hubs like Hong Kong. Hong Kong has an open licensing regime with no limit to the number of new licenses and has reformed its regulations to make it easier for interested parties to install cables with or without affiliated data centers.

Marine regulations can also affect cable installation and repair. For instance, Indonesia’s Shipping Law requires all vessels including cable ships operating in Indonesian waters to have Indonesians as majority shareholder. The U.S. Trump administration attempted to revise the Jones Act interpretations to require cable ships stopping at U.S. ports to be built in U.S. shipyard with U.S. citizens comprising at least 75% of crew members and vessel ownership, but halted the change after receiving industry complaints.

Growing role of Chinese investments

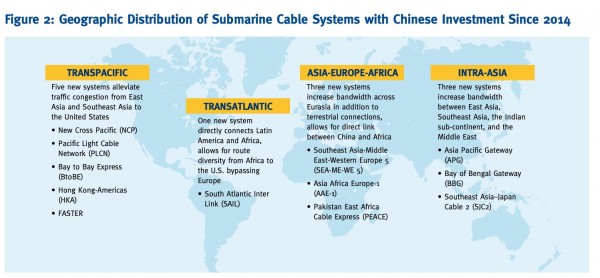

China has significant interests in cable infrastructure to meet its connectivity demand and increase connectivity in other emerging markets. According to the Chinese Ministry of Industry and Information Technology (MIIT), only ten international submarine cables connect to mainland China, lagging far behind advanced economies like the United States (80 submarine cables) and Japan (23 cables). In 2017 total international bandwidth (including submarine and terrestrial cables) was 7.3Tbps, which on a per capita basis was less than one-twentieth of the United States’. The 13th Five-Year National Information Plan (2015-2020) aims to increase total international bandwidth to 20Tbps by 2020. The Belt and Road Initiative (BRI), announced in 2013, also pledges to support cable development as part of the 21st Century Maritime Silk Road. Twelve new cable systems either completed or with contract in force since 2014 have received Chinese investment. Emerging markets show rising importance in the geographic distribution (Figure 2).

While carrier consortiums drove most new cable development with Chinese investments, other actors also participated. Major Chinese carriers, China Unicom, China Telecom, and China Mobile all participate in multiple consortiums. In a few cases consortiums include global online content providers like Facebook, Google, Amazon and Microsoft. Financing sources also include China Construction Bank, the Export-Import Bank of China, private Chinese investors, and cable suppliers and manufacturers like Huawei Marine and Hengtong Group (HTGD). The China-led Asian Infrastructure Investment Bank (AIIB) has financed terrestrial cables but not submarine ones. Unlike their western counterparts, Chinese online content providers have not directly financed submarine cables. They primarily buy capacity from infrastructure providers. For instance, Alibaba partners with Tata Communications to deliver cloud access to international consumers. Future direct participation is however possible, as Alibaba, Tencent and Baidu became China Unicom shareholders in 2017.

Protecting Cable Infrastructure and Managing Cyber Risks

Robust domestic regulations are crucial for cable protection. While states may worry about deliberate attacks (pioneered by Britain cutting telegraph cables to Germany in World War One), fishing and ship anchoring is responsible for about 70% of cable faults. Without regulatory oversight and public awareness, fishermen and vessels may lack the incentive to take precautions. For instance, in 2006-07 Vietnam allowed fishermen to salvage undersea copper cable laid before 1975 to sell as scrap. Fishermen ended up stealing fiber optic cables of about 43 km (27 miles), leaving the country with just one international cable. In international waters, current international regimes offer limited protection for cables. The 1884 Convention for the Protection of Submarine Telegraph Cables, in force for thirty-seven state parties, does not apply to most emerging markets. The United Nations Convention on the Law of the Sea (UNCLOS), ratified by 167 state parties, contains provisions on cable protection, yet states have significant discretion in interpreting them in practice, and the United States is a major country that has not ratified the treaty. Competing maritime claims in areas such as the South China Sea also increase the complexity of intergovernmental coordination.

Cybersecurity is another enduring concern in cable infrastructure. For instance, Edward Snowden’s revelations about the U.S. National Security Agency tapping undersea cables led to the BRICS (Brazil, Russia, India, China, South Africa) cable proposal, though the project stalled in 2015. Chinese suppliers can also face suspicions. For instance, Huawei Marine is a joint venture established in 2008 between China’s Huawei, a global telecom equipment provider, and UK-based Global Marine Systems, a marine engineering company involved in cable installation since the first cable in 1850. The firm has gained market share by offering new technologies, flexible design for operator needs and cost-efficient installation, and has completed 90 projects across Asia and the Pacific, Europe, the Americas, the Middle East and Africa. Measured by installed cable length, Huawei Marine ranked 4th globally in 2013-17, behind UK-based Alcatel Submarine Networks (part of Nokia), U.S.-based TE Subcom, and Japan-based NEC. However, in 2018 Australia blocked Huawei Marine from supplying the Coral Sea Cable System connecting Australia to Papua New Guinea and the Solomon Islands. Alcatel and Australia’s Vocus Group have been contracted to lay and operate the cable.

New connectivity also brings dangers of digital exclusion and cybercrimes. Countries lacking diversified carriers or landing stations have higher risks of deliberate or accidental shutdown of international connectivity. Cybercrimes gravitate towards the place of least resistance, disproportionately affecting emerging markets with inadequate cybersecurity infrastructure.

Recommendations

1. Interested parties need to proactively identify strategically located cable systems that enhance international connectivity to emerging markets and explore financing solutions from diverse sources. Regulators need to develop efficient licensing and effective regulatory structures to reduce approval times and decrease political risks for investors and suppliers.

2. Regulators need to enhance domestic regulations and education campaigns to prevent human damage to cables in territorial seas. Intergovernmental coordination in international institutions or treaties involving emerging economies can improve cable protection in international waters.

3. Stakeholders need to develop public awareness, technical skills, and regulatory capacity to address vulnerabilities such as cyber attacks, cybercrime and Internet shutdown.

4. Hong Kong should maintain its advantage as an international digital infrastructure hub and seize opportunities from rising demand for network infrastructure, financing, and legal and management expertise. For emerging economies, Hong Kong can provide an international gateway while serving as a role model in regulatory efficiency, cable protection, cybersecurity and inclusion.

About the Authors

Yujia He is a Postdoctoral Fellow jointly appointed with the Institute for Emerging Market Studies and the Institute for Advanced Study at HKUST. Previously she worked in Washington D.C. for the Atlantic Council’s Scrowcroft Center for Strategy and Security, and for the Wilson Center's Science and Technology Innovation Program. She is interested in digital economy development, international political economy and science and technology policy. Her research has appeared in Resources Policy, International Journal of Emerging Markets, and several think tank reports. Her degrees include PhD in International Affairs, Science and Technology (IAST) from the Georgia Institute of Technology and BS in Chemistry from Peking University.

Get updates from HKUST IEMS